Seeking Alpha

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

Amazon (AMZN) didn't make a dime in 2012. Investors have been very forgiving of the profit deficit and instead have focused on Amazon's revenue growth.

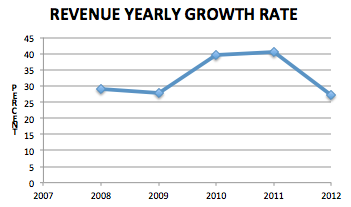

Indeed, sales have been increasing. Take a look at yearly revenue growth over the last five years:

(Sourced from 10ks.)

Yet, there's a problem. While revenue growth had been accelerating year after year, up 28% in 2009, up 40% in 2010, and up 41% in 2011, lately Amazon has taken its foot off the gas pedal. Revenue growth has stopped accelerating. This year, sales grew 27%, a far cry from the roaring 41% increase of 2011.

But hey, one year. What's that? One year doesn't make a trend.

However, there is a deeper more firmly entrenched pattern, a lot more disturbing than the yearly revenue growth. Take a look at the last seven quarters. Every earnings season growth has been slowing down.

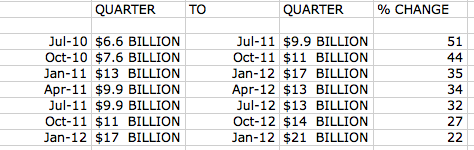

In fact, revenue growth has slowed in each of the last seven quarters. Each earnings season has brought a smaller sales increase from the year-ago quarter. Sales grew a whopping 51% in July 2011. Growth has decelerated from there. Last quarter, sales grew a much lower 22%.

Here are quarter sales and the percentage change from the year-ago quarter. Note the steadily growth deceleration:

(Sourced from 10Qs.)

If the pattern holds, the next few quarters will see sales growth trend below 20%. You can see the trend in the graph below:

(Click to enlarge)

Don't know about you, but seven quarters of decelerating sales is worrisome. This isn't the shoot-the-lights-out growth you'd expect from a company with a current PE of 179.

So what does Amazon say about its future revenue growth? From their conference call, Amazon expects $15 billion to $16.6 billion in sales next quarter, a 14% to 26% increase. The midpoint of the range is 20%. That would make the 8th quarter of decelerating revenue growth.

If the on-line seller is taking share and growing to the sky, why has Amazon's sales growth been slowing down?

Amazon's Growth Rate Is Overpriced Compared To Other Stocks

Amazon has a forward PE of 72 with slowing revenue growth. I ran a screen for all companies with over a billion dollar market cap meeting the following criteria:

- Revenue growth TTM over previous year TTM of at least 27%.

- Revenue growth latest quarter over year-ago quarter of at least 22%.

Only 16 companies had forward PEs of 40 or more. By far, Amazon had the lowest revenue growth of the cohort. Yelp (YELP), Palo Alto Networks (PANW), Splunk (SPLK), ServiceNow (NOW), Zillow (Z), Level 3 Communications (LVLT) and LinkedIn (LNKD) grew revenue growth for the year and quarter greater than 60%. Amazon's growth pales in comparison to this bunch.

However, there were 117 companies with forward PEs of 30 or less. With its declining revenue growth, Amazon more appropriately fits into this group.

Bottom Line

No profits. Decelerating revenue growth. Crazy-high valuation. Until Amazon gets its sales mojo back, it deserves a pull back.

ETF Alternatives

sponsored by

sponsored by

Otherwise, how could Amazon be leading among too many e-sites?

I predict that 7 years out AMZN will still be a company but it'll trade at Walmart's P/E and will have experiened a catastrophic loss of market cap.

I think amazon is an overweight monkey in a room with large gorillas. I don't care how good their robots are and how great their supply chain is. Amazon is a job destroyer and they are a direct competitor for the same vendors they host on their marketplace. I venture to say that if ebay started selling the same goods their vendors sell then ebay would become a penny stock quickly. Ebay will not do that but amazon does and amongst amazons vendors there are few that love amazon. Their vendors would sooner throw amazon under the bus then save them from being run over. Ebay on the other hands has a large majority of dedicated vendors. Recent reports stated that amazons marketplace is making progress and expanding. We will see how fast their marketplace shrinks when they are forced to collect sales tax everywhere.

Their international effort as valiant as it is will face problems from overseas governments. The biggest problem with amazon is that their competitors, large corporations and small businesses, the mom and pop stores, the fly by night vendors would rather see them fail then succeed. This will severely impact amazons ability to raise margins. Once the price advantage goes away amazons core customer will shift to places and vendors they love instead of amazon. Amazons core dedicated audience is the end user. Companies, ceo's, business owners simply want amazon to vanish because amazon is a disruptive business but while the price is cheap why not save some money?. There is nothing revolutionary about putting people out of work while not making any money in the process.

Amazon and its disruptive effort is allowed to exist purely on the backs of misguided investors who have the benefit of luck on their rear and headwinds in front. I think it is amazons lofty p/e that propels the stock forward instead of its disruptive strategy. Like throwing more fuel on a fire. Eventually the fire burns out, no puns intended. I am short amzn as of 275$.

I mean really, the company is priced hundreds times earnings all because one day it will rule the world? you have to be profitable and make money to rule the world. one day they will make profit? wake me when they do. I can then shop elsewhere. One day they will be a job creator? I think to create jobs you have to make money otherwise you are putting people who make money out of business and out of jobs. UPS and fedex are few corporation that probably love amazon but even they would rather amazons business go to smaller companies where the profit for the carriers is higher. Self fulfilling prophesy. When you put everyone out of business you have no customers left.