Seeking Alpha

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

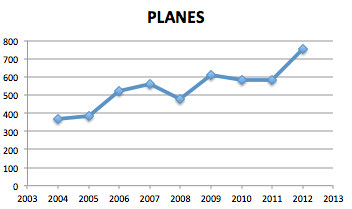

Boeing (BA) has been selling more planes each year. That's easy to see. The company gives you those numbers at the end of every year. I've lumped together all deliveries: commercial, defense, space and security under "planes":

I'm giving Boeing an A for increasing volume. Even after the gigantic problems getting the 787 off the assembly line, the company doubled deliveries in eight years. I like that.

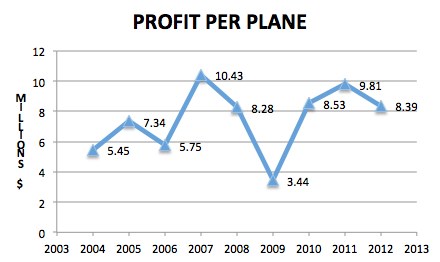

Yet, how much did Boeing actually make off of each aircraft? Boeing isn't going to give anybody that info. No way. Too proprietary. Yet, it's easy to derive.

The magic formula: Operating income divided by the number of deliveries. That gives you Boeing's unit profit per delivery. Operating income is easy to find. And as we noted above, Boeing tallies its deliveries at the end of each year.

For 2012: 601 commercial planes and 154 defense, space, and security deliveries. Grand total = 755.

Plugging the delivery total into our equation: $6.311 billion operating income per 755 deliveries = $8.39 million dollars a plane. $8.39 million is a lot of money to make (before taxes, of course -- after, it's not quite as much).

Let's run those Boeing unit profits over the last seven years:

I think we can throw out 2009. That was the craziest year: economic disasters and hideous mechanic striking. Kick that out. What we're left with is a unit profit that is trending downward -- just a little. Still, $8.39 isn't bad compared to 2004 and 2006 and the nasty 2009 (but I promised not to mention that, didn't I?).

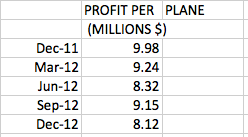

Let's drill down and look at each of the last five quarters to see if this is an unpleasant trend:

Oops. Profits per plane have been falling for the last five quarters. The trend going into 2013 does not look good from a unit profit point of view.

With the Dreamliner battery woes and sequestration on its way, this may be the tip of the iceberg. Unit profits dropped even before the 787 battery problem. We can expect that declining unit profits are coming as Boeing tries to find a battery fix. ANA, Japan's largest airline group, has lost $15 million so far, a bill that will probably land on Boeing's desk. Looks like it's going to be a challenging year for Boeing.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

ETF Alternatives

sponsored by

sponsored by

Let’s put some of these numbers in context. Boeing has 800+ orders for the 787, which has been on sale for about a decade now. That’s considered to be great, for a twin isle plane. Last year, 2012, Boeing had 1124 net orders for the 737 (-11 net for the 787, by the way). 415 of the 601 commercial aircraft delivered last year were 737s.

Boeing and Airbus orders are often conflated with sales but orders are not at all what layman would think of as sales. EADS/Airbus has succeeded in getting the business press to hype the yearly order totals while at the same time diluting their “worth” by stretching the orders far out into the future and also counting many orders that never materialize (normal, but not to the extent Airbus has taken it to). This allowed Airbus to project the perception that they were much larger than they were, many years ago, and also to make them look much more successful than Boeing. Both those misperceptions are easily shown to be false by simply looking at the financial numbers for the companies. Airbus won the yearly orders race for 10 straight years and yet, in 2012, Boeing delivered more planes than Airbus – doesn’t quite add up, does it?!

Don’t get me wrong, Airbus is a great company and has had amazing success in a very complex business, in a short span of time. But Boeing has done quite well themselves and, I believe, the 787 will be a huge success for many years to come.

Thanks for the information.

The article discusses deliveries, not orders.

You'll note that, in Dec 2012 quarter, Boeing delivered 23 787s and 105 737s while in Dec 2011 quarter, Boeing delivered 2 787s and 91 737s.

Yet, despite delivering a much greater number of the more expensive 787s, average aircraft profits dropped by $1.86 million a plane.

While there are lots of moving parts (plane mix, timing of payments), the unit profit trend is not good.

http://bit.ly/VcuSMc