Seeking Alpha

Too Late To Sell? Look Who's Trying To Dump J.C. Penney

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

J.C. Penney (JCP) hasn't been doing well. Store traffic last quarter was down 17% year over year and comparable store sales plunged 32%, confirming my impression that this J.C. Penney has become more of a museum than a retailer.

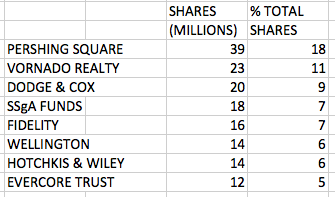

It looks like the only people buying J.C. Penney have been large mutual funds. Unlike shoppers, they really like J.C. Penney. Out of 219 million shares outstanding, eight institutions own 156 million shares, or 69% of J.C. Penney. That's what I call concentration.

Look at the list (courtesy of Morningstar.com):

Unfortunately, most of these institutions didn't sidestep the dismal performance of J.C. Penney's stock. Ackman's Pershing Square still owns the same 39 million shares it did years ago. That's unfortunate, as shares have dropped 57% over the year. Too bad the funds didn't heed my bearish call back in March 2012.

It looks like one institution is trying to dump its shares. According to CNBC, Vornado (VNO) reportedly is shopping its stock, helping to drop J.C. Penney another 2% after hours.

Interestingly, J.C. Penney's Savings, Profit-Sharing Plan and Stock Ownership Plan has been lightening up on its holdings for several years. According to the SEC documents, the Plan has been decreasing its shares, reporting 16 million shares in December 2010, 14.6 million inDecember 2011, and 11.7 million last December. They may be the smartest ones of the bunch.

Too late to sell? Not by a long shot.

Additional disclosure: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. We do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for his specific situation.

ETF Alternatives

sponsored by

sponsored by

J.C. Penney Company Inc.

6,542 people get email alerts on JCP

Get email alerts on JCP

I still think JCP will pull through.

1) The largest holder, Pershing Square, purposely bought a large stake *because* of the poor performance, *before* your "bearish call back in March 2012."

2) He did this to force on a new CEO to do massive cost cutting and turn around the company

3) The CEO has been incentivized for 3 years (it's only been a bit over a year?) in regard to stocks.

4) Based on the time needed for a turn around, and because of how the CEO has been incentivized, Pershing Square said they are waiting 3 years for a turn around.

In contrast, had they sold on my sell recommendation last March, they would have saved themselves over $800 million or 60% of their holding.

Why they decided to totally revamp the company is beyond me. Better inventory management, incentivizing staff, improving store appearance, closing underperforming stores and maybe trying out Johnson's ideas in a few model stores...that was the way to go.

JCP only needs to attract back these shoppers with some good promotions. Then they'll see the changes and appreciate the leadership of the CEO. Very tasteful and forward looking.

9